Who we are

Company background

HASL Asia enjoys a unique blend of Eastern and Western heritage inherited from our Mainland China and UK background

Awards and recognition

Heng An Standard Life Asia earns industry recognition for its professional services and products

What we offer

Hong Kong New Capital Investment Entrant Scheme

Our investment-linked assurance schemes (ILAS) are permissible investment assets under the new CIES.

Investment-linked insurance plans

Our investment-linked insurance plan may help you capture market potential and cater for your insurance needs

CareMore

Enjoy peace of mind for you and your family with extensive health coverage

MoreAcademy

Education series

Gain more understanding about your insurance with our guides, from basic principles to managing investments over the long term

Market watch

Follow trends and get the latest information about various industry sectors and behaviours

Investment information

Professional investment management

Our investment-linked insurance plans offer a wide range of investment choices linked to underlying funds managed by reputable investment managers

Notice in relation to investment choices

Stay fully informed on your investments with the up-to-date notices

Our Investment Choices

Investment involves risks. Past performance is not indicative of future performance. For details of the risk factors, fees and charges of the plan, please refer to the offering documents of the relevant plan.

Help and support

Download hub

Access forms to switch policies, sign up for investments, change personal information

Go green

Go green, go paperless Support environmental friendliness by moving away from paper to electronic notices

Market watch

High Yield: Charting a Steady Course Through Roiling Seas

Issue date: 2023-07-07

Barings

Banking stresses added volatility to first-quarter markets already coping with rising rates and recession fears. Still, with corporate fundamentals sound, high yield investors and issuers are more cautious than fearful.

Triggered by the failure of Silicon Valley Bank and Signature Bank, many equity investors fled to safety in March and created volatility rarely seen in fixed income markets. As U.S. Treasury prices jumped, option-adjusted U.S. high yield spreads widened, then subsequently declined again in a matter of weeks. Despite unprecedented volatility, high yield investors largely stayed put and did not succumb to panic, as evidenced by the market’s wafer-thin volume and modest outflows from high yield mutual funds. Waiting out the turmoil seemed to be the playbook for investors and issuers alike.

Market Drivers

Concern over the health of the banking system was a new factor driving volatility toward the end of the first quarter, but the uncertainty that pervades the market is a continuation of the mood that has prevailed since the U.S. Federal Reserve began raising interest rates in March 2022. Since then, we have emphasized a focus on higher-rated issues and careful attention to market niches and credit selection. We have no direct high yield exposure to the banking industry in the U.S. and Europe, as the industry’s opacity regarding its balance sheet structure inhibits the thorough credit analyses we require before investing. Index exposure to banks is low (<1%) in U.S. high yield indices, however much larger in Europe at approximately 13%.1

Through the roller coaster of volatility, the technical backdrop has remained steady in high yield and loan markets. In the latter, the paucity of new supply and high levels of cash among managers have kept the market firm. At the same time, the fundamental environment has turned slightly more negative. In the U.S., the effect of last year’s rate hikes is beginning to be felt throughout the economy, affecting aggregate demand and raising costs. Add higher outlays for labor, and many corporations will likely have a harder time passing along their higher costs to customers. Lower reported first- and second-quarter earnings in some cases could be significantly below expectations, exacerbating volatility.

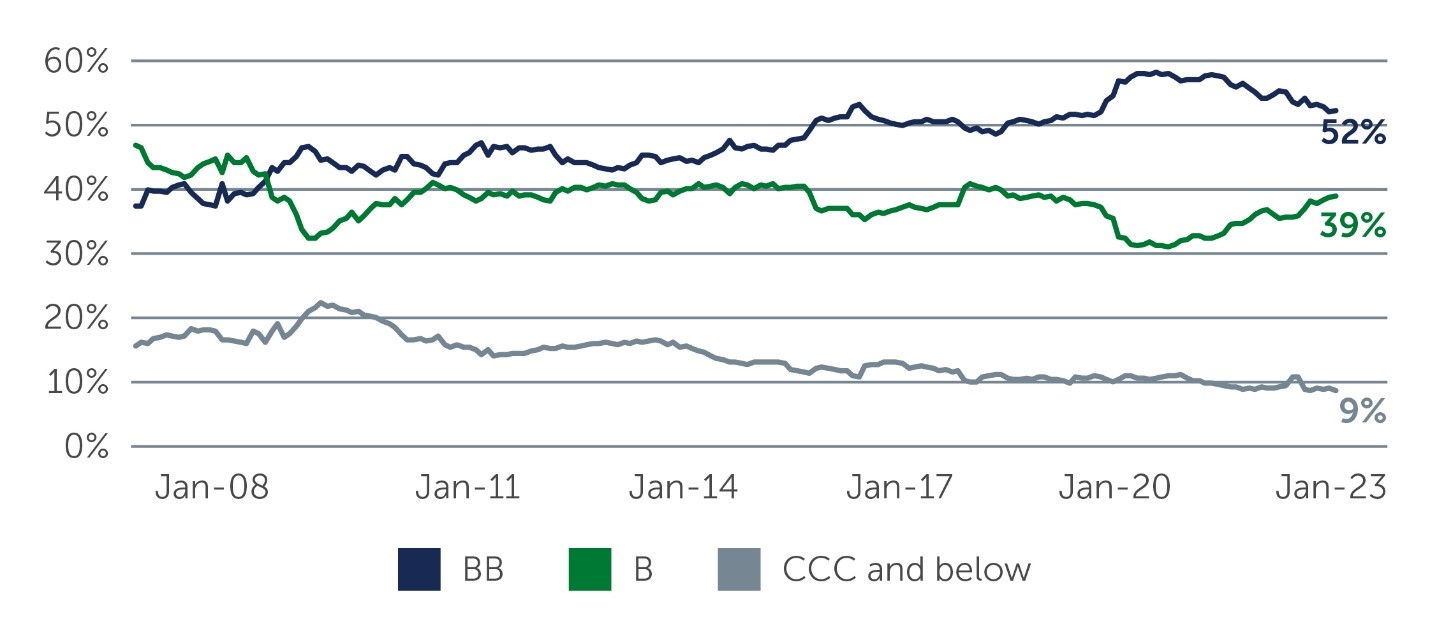

In the current uncertain environment, companies that are not highly leveraged and have ample cash and/or access to capital are best positioned to ride out any difficulties that emerge. High yield issuers overall, fortunately, are in a stronger financial position to ride out this period than they were pre-pandemic, since in the aggregate they have lower leverage and higher interest coverage. Notably, the credit quality of the global high yield bond market has also improved considerably over the past 15 years—BB issuers comprise 52% of developed markets high yield today, while single-B companies make up 38% (Figure 1).

Figure 1: A higher-quality market

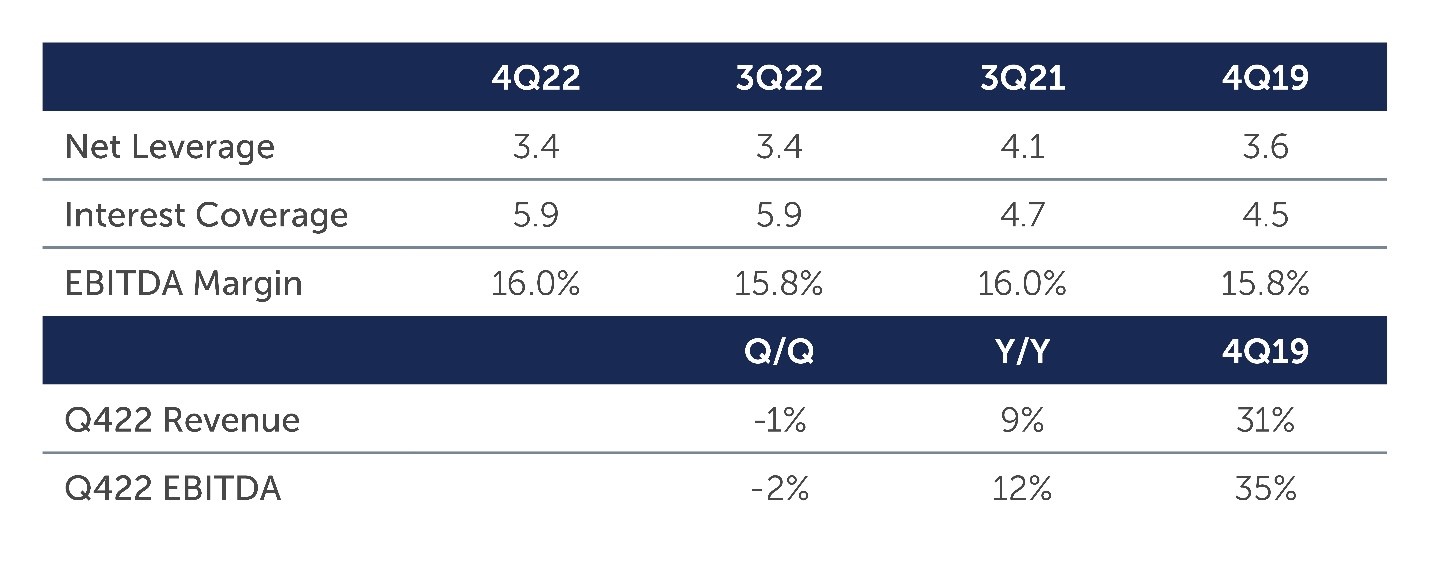

Default rates have remained very low in recent years and while defaults are likely to increase if the economy slows and credit conditions tighten, the higher quality of today’s market, the stronger prevailing credit fundamentals (Figure 2), and limited near-term re-financing needs should keep defaults near historic averages. Rigorous, bottom-up credit selection and a bias toward higher-rated issues remain key to managing default risk.

Figure 2: HY corporates are starting from a strong base

Attractive Total Return Potential

Uncertainty about the future course of the economy and interest rates is likely to continue, making short-term forecasts challenging, especially considering market sentiment prone to skittishness. But reviewing the market’s certainties and looking beyond the current turbulence can provide a case for high yield investing on an absolute basis as well as in comparison to equities.

At the higher end of the quality spectrum, periods of mild recession in the past have had little impact on high yield issuers. In fact, investors who have stayed invested in high yield through periods of volatility, and even economic decline, have historically been rewarded with attractive, long-term returns. This is partly because high yield, unlike equities, does not require strong economic growth to perform well. Rather, what matters more in high yield is an issuer’s ability to continue to meet the interest payments on its outstanding debt obligations. Slow GDP growth, or even a short period of mildly negative growth, is unlikely to drive significant increase in defaults—particularly across a higher-quality market with solid underlying fundamentals.

In the meantime, in addition to offering attractive coupon payments, higher-quality bonds have traded at discounts to par, providing the potential for capital appreciation as maturity nears and eliminating the need to take on excessive risk by dipping into lower-quality credits.

The key point for investors is that if they can remain patient and are willing to hold on through roiling markets, potentially attractive total returns await.

Figure 3: Valuations at current levels are rare and have historically led to strong double-digit returns over the following 12 months

1Source: Bloomberg. Europe data for ICE BofA Euro High Yield Constrained Index, U.S. data for ICE BofA U.S. High Yield Constrained Index. As of March 22, 2023.

Important Information The document is for informational purposes only and is not an offer or solicitation for the purchase or sale of any financial instrument or service. The material herein was prepared without any consideration of the investment objectives, financial situation or particular needs of anyone who may receive it. This document is not, and must not be treated as, investment advice, investment recommendations, or investment research. In making an investment decision, prospective investors must rely on their own examination of the merits and risks involved and before making any investment decision, it is recommended that prospective investors seek independent investment, legal, tax, accounting or other professional advice as appropriate. Unless otherwise mentioned, the views contained in this document are those of Barings. These views are made in good faith in relation to the facts known at the time of preparation and are subject to change without notice. Parts of this document may be based on information received from sources we believe to be reliable. Although every effort is taken to ensure that the information contained in this document is accurate, Barings makes no representation or warranty, express or implied, regarding the accuracy, completeness or adequacy of the information. Any forecasts in this document are based upon Barings opinion of the market at the date of preparation and are subject to change without notice, dependent upon many factors. Any prediction, projection or forecast is not necessarily indicative of the future or likely performance. Any investment results, portfolio compositions and/or examples set forth in this document are provided for illustrative purposes only and are not indicative of any future investment results, future portfolio composition or investments. The composition, size of, and risks associated with an investment may differ substantially from any examples set forth in this document. No representation is made that an investment will be profitable or will not incur losses. Where appropriate, changes in the currency exchange rates may affect the value of investments. Investment involves risks. Past performance is not a guide to future performance. Investors should not only base on this document alone to make investment decision. This document is issued by Baring Asset Management (Asia) Limited. It has not been reviewed by the Securities and Futures Commission of Hong Kong. 23-2837854 |